Election Years and Equity Volatility: A Quantitative Perspective

Political cycles have long shaped market psychology. U.S. presidential elections, in particular, represented major macro events with potential to alter fiscal priorities, regulatory focus, and global relationships. Options markets, through instruments like the CBOE Volatility Index (VIX), revealed how investors prepared for that uncertainty. In this research project, I examined whether election years consistently heightened volatility pricing. I focused on October, a month that has historically served as a turning point for risk sentiment and has often aligned with severe market stress episodes.

Descriptive Patterns

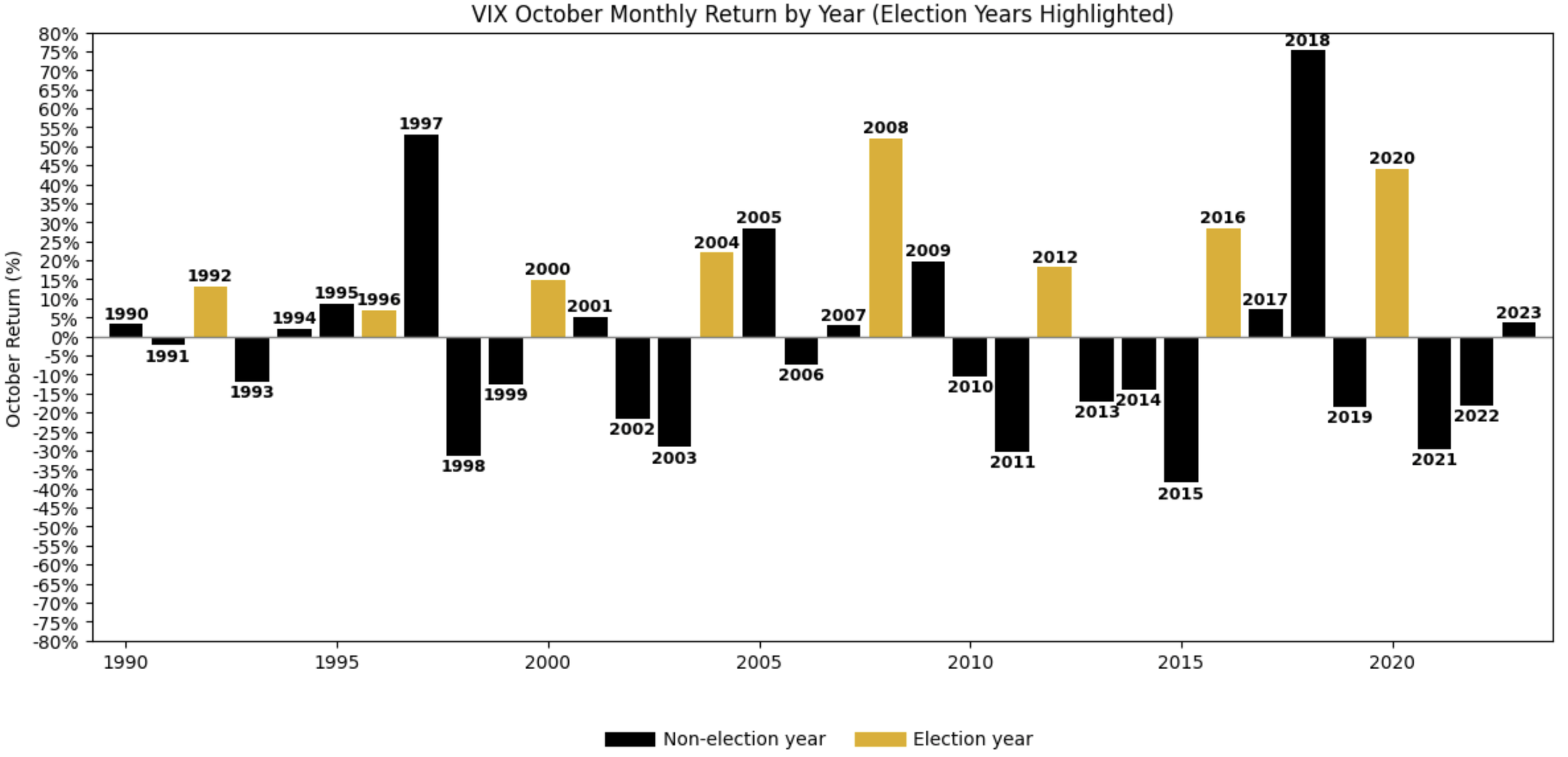

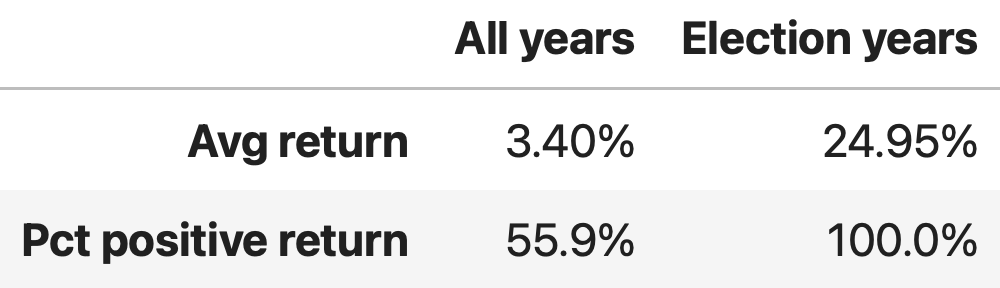

The historical pattern was immediately visible in the data. Election-year Octobers consistently exhibited stronger volatility pricing than non-election years. In statistical terms, the mean October VIX return in election years was roughly 25%, compared with just over 3% otherwise. Additionally, every election-year October posted a positive return, whereas only 56% of non-election years did so. These simple differences already hinted that political cycles may have operated as a structural catalyst for volatility repricing.

Methodology

From this raw panel, I constructed a series of monthly endpoint observations and computed October returns as the percentage change from the final trading day of September to the final trading day of October in each year. The full workflow was coded in Python and organized in a reproducible structure within a GitHub repository (see top of article). All code, data ingestions, variable construction, and outputs were managed inside a Jupyter Notebook, enabling transparent iteration and review.

Election years were encoded as a binary indicator corresponding to the presidential cycle calendar {1992, 1996, 2000, 2004, 2008, 2012, 2016, 2020}. To evaluate baseline conditions that might confound results — such as already-elevated volatility — I included September-end VIX levels as a control in alternate specifications. Through this approach, I ensured that differences attributed to election risk were not simply reflections of high prior volatility.

The statistical testing proceeded through three complementary channels:

Ordinary Least Squares measured the magnitude of the election-cycle impact on October returns.

Penalized logistic regression (ridge) assessed whether election status increased the likelihood of a positive October return.

Bootstrap resampling (10,000 draws) produced non-parametric confidence intervals to confirm robustness independent of modeling assumptions.

Model output was evaluated using coefficient estimates, p-values, odds ratios, and confidence interval coverage. To reduce sensitivity to outliers, I analyzed distributions of resampled means rather than relying solely on asymptotic inference. The workflow closely mirrored the empirical practices used in institutional macro research environments.

Results

The results were consistent across all methods. The baseline OLS regression estimated that election years corresponded to roughly a +28 percentage-point increase in the October VIX return (p ≈ 0.007). Including September volatility levels as a control yielded nearly identical inference, indicating that the effect was not simply driven by pre-election shocks. In the penalized logit model, election years increased the odds of observing a positive October return by nearly 7x (p ≈ 0.09). Bootstrapping reinforced these findings: only election-year Octobers produced a mean return statistically distinguishable from zero at the 95% confidence level.

These converging results pointed to the same structural conclusion: volatility markets systematically priced uncertainty before election outcomes were known.

Interpretation

This pattern highlighted that option-market participants did not wait for definitive results. They hedged in advance of political decision points, bidding up implied volatility as policy scenarios diverged and risk preferences tightened. The VIX functioned not merely as a fear gauge but as an instrument for encoding the pricing of political change. Consistent with macro-finance theory, investors assigned tangible value to uncertainty itself, particularly when multiple governance paths carried materially different consequences for growth, taxation, regulation, and geopolitical stance.

Research Contribution

By combining economic intuition with empirical testing, the project helped substantiate a commonly held belief — that presidential elections elevate equity-market anxiety — with quantifiable and statistically robust evidence. More importantly, the methodological rigor ensured that the conclusion rested on reproducible measurement rather than headline-based observation. The notebook-driven workflow, structured repository, and bootstrap-supported inference aligned with the analytical discipline expected inside volatility and macro hedge funds, where data reliability and robustness matter as much as raw signal discovery.

Conclusion

The findings illustrated that political uncertainty reliably transmitted into volatility markets, especially in October ahead of U.S. presidential votes. Rather than responding exclusively to post-election news, markets priced in the uncertain transition itself. This project provided a useful blueprint for how macro events can be transformed into tradable insights: form a hypothesis grounded in real-world incentives, build a clean dataset, evaluate sensitivity across multiple models, and confirm persistence through simulation. From both a financial and methodological standpoint, the work demonstrated that political cycles are not merely civic milestones — they are predictable volatility events embedded within the broader market regime.